Buying your own home will without a doubt be one of the biggest decisions that you take in your life. At one point in our lives or another, don’t we all dream of having our very own home, one that we can design and decorate exactly the way we please? If purchasing a home has ever crossed your mind, we are sure you must have been curious enough to do some basic research too. If not research, you must have at least discussed the idea of purchasing a home with your family and friends. Ask anyone who has been a part of the home buying process, and they will instantly tell you how important a role financial planning plays in your final decisions.

You cannot succeed in buying the right home for yourself if you are impulsive or under pressure. One of the greatest ways to ensure you make this decision with a clear mind is if you are well researched and aware of the elements that go into this process. Since this is an extremely financially binding decision, you need to ask yourself - can you even afford a home?

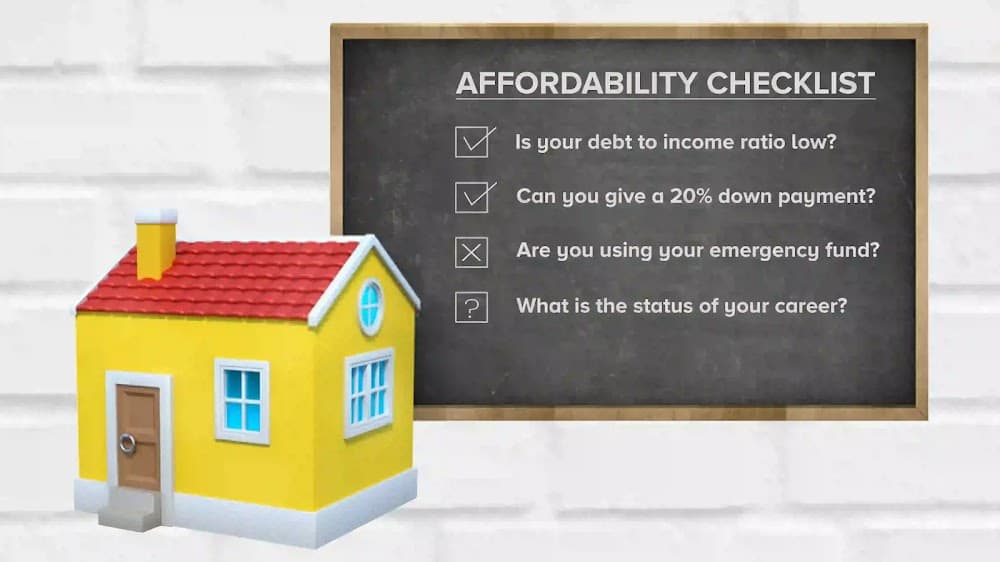

Affordability goes way beyond just having a basic income and the always open option of getting a home loan. You need to take some time out and ask yourself some questions that will determine if you are financially ready for this next big step in your life. It is not that big of a task. To make it easier for you, we have collated a list of questions that you can ponder upon and figure out your overall financial status when it comes to home buying.

Are you using your emergency fund to make the down payment?

If your answer to this question is “yes”, then you might not be ready to purchase a house yet. Using your emergency fund or digging into your liquid assets to pay off the down payment is not worth it. Don’t make a rash money decision as this emergency fund might be of use to you in the future. In the event of an accident, loss of job, or any other tragic life event, it is only the emergency fund that will help you through it by easing your stress.

Also Read: Financial Question Answers Before Buying Home

Are you spending more than 30% of your income to buy the house?

The bad news is that if you end up spending more than 30% of your income on buying this house, this house might just be slightly more expensive than you can afford. You are in good shape if you can afford to keep your house payments to under 30% of your total income. Just think of the amount of money you can spend on traveling and retirement! It happens more than often that most of us get overconfident and end up spending a large chunk of our income. However, this harms our standard of living and lifestyle in the future.

What is the status of your debt to income ratio?

Calculate this ratio by dividing your monthly income by the debt payments that you make each month. Your chances of getting approved for a home loan will reduce significantly in case you have a high debt to income ratio. Statistically, the highest ratio that is generally approved goes up to 43%. Increasing your income or paying off your debts as soon as possible are the only two solutions for individuals that are struggling with a high debt to income ratio.

Are you even in the condition to make a complete down payment?

If fulfilling the down payment requirements is not a problem for you, then you might just be ready to buy your own home! A smart buyer has saved for the down payment amount and does not have any second thoughts about paying it off. If at any point in time you hesitate to pay the down payment in full, stop and reflect. Ask yourself if this is the right time to spend this huge amount of money. After all, a down payment is just the beginning when it comes to purchasing a home.

Have you taken into account the future expenses?

A smart buyer needs to research and be aware of more than just the purchase price. Once shifted to your new home, you will have to spend money on both maintenance and added utilities. Have you made a list of the utilities that you would essentially need on a daily or even monthly basis? If your homeowner’s insurance is not yet in place, then factor that in too. On top of all this, you will also spend a large chunk of your money on paying off your mortgage every month.

Keep in mind that your mental preparedness is as important as your financial preparedness. Once you are sorted with the financial checklist mentioned above, make sure you reflect on how you feel about this big decision of your life. In the end, if you are not mentally prepared to invest a big amount of your funds towards buying a home, being financially secure won’t be much of a help. If you need some extra assurance to be 100% sure, you can also glance at some of the key financing considerations to take into account before signing the final documents for your house purchase.

With housing prices on the rise and the demand increasing by the day, using this checklist will bring you one step closer to finally buying your dream home!