The process of buying a property and homeownership for many is undeniably a proud feeling and one of the most celebrated events. There are various payment plans one can opt for. Considering the income ranges, it is important for you (as a homebuyer) to understand each kind of payment plan and calculations.

For real estate developers, the competition is fierce. When a potential homebuyer approaches a specific developer, the latter demonstrates the product's

Quality

Types of amenities

Safety features

Location advantage

Connectivity

Once the potential buyer is convinced, the price of the product (as home) and its payment plan are the last two deciding factors for a deal to succeed. Attractive payment plans do encourage people to buy properties. Hence, check what all payment plans are offered in India and how they can help you avoid confusion

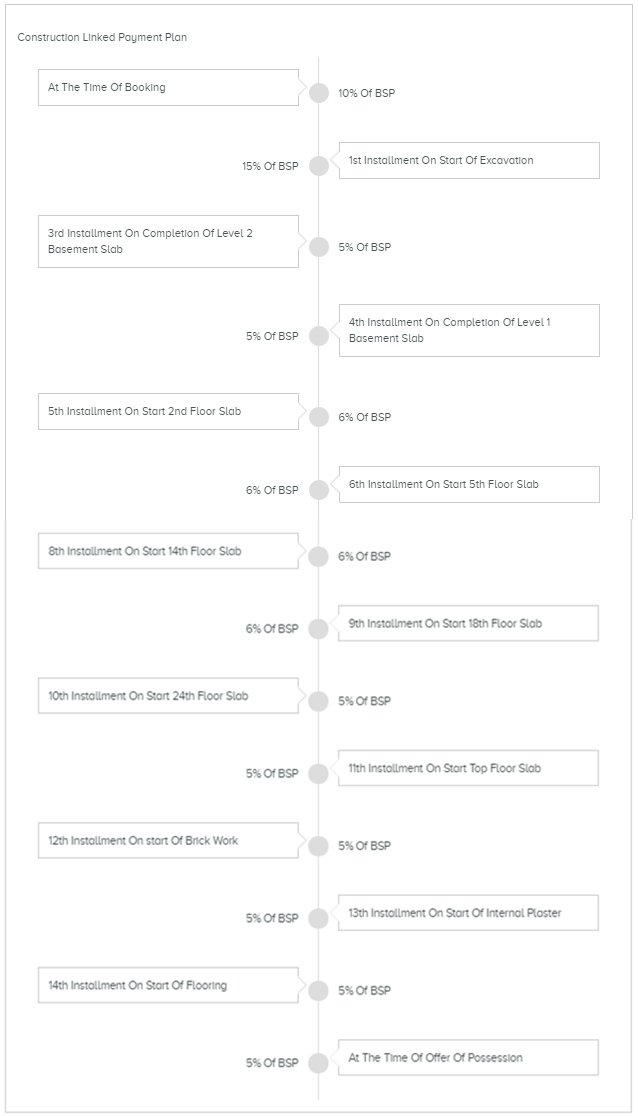

1. Construction Linked Plan is a popular choice

The three parties are involved in Construction Linked Plan (CLP) - Bank, Buyer and Builder. A homebuyer approaches the bank, and the latter pays out the amount to the builder on behalf of the homebuyer until the possession of the concerned property.

Disbursement of the amount by the bank depends on the construction progress carried out by the builder. Whenever a section of the project is completed, for instance, a floor or other types of infrastructure, the bank pays the pre-decided amount to the builder.

The chart below is an example of a Construction Linked Plan of Shri Radha Sky Park (residential project in Greater Noida) by SHRI Group

Merits of CLP

While the bank pays the amount to the builder, the buyer gets sufficient time to save his/her income.

Only after possession of the property, the buyer needs to repay the amount to the bank.

Middle-class being a dominant population in India, this mode of payment is beneficial to them as it does not demand big financial commitments at once.

Demerits of CLP

It cannot safeguard the buyer against the construction delays of the project.

EMIs to the bank is required to be paid only after the possession of the property. However, the buyer has to pay the rent of the current residence and interest component of the loan.

The builder may draw 90 to 95 percent of the amount from the bank and delay the final handover of the project by a couple of years. The buyer is likely to suffer from struggling to possess the property fully and will have to bear the burden of loan interest.

2. Down Payment Plan (DPP)

Under the scheme of down payment, the buyer usually pays 10% of the total cost of the property as down payment, at the time of its booking. Another 70%-90% is paid within a given time-frame (usually 30-60 days) and the rest of the amount is paid at the time of possession.

The chart below is an example of a Down Payment Plan of Godrej Summit (residential project in Gurugram) by Godrej Properties

Merits of DPP

As you pay a high amount within a short period, you get the advantage of asking for a discount of around 10%-15% on the total price of the property to the builder.

Demerits of DPP

In case the construction gets delayed, recovering money from the builder can be a challenge.

3. How Subvention Payment Plan (SPP) works

Step 1. The procedure of this payment plan begins when the buyer pays an initial booking amount or the down payment of usually 10%-15% of the total amount of the property.

Step 2. The bank agrees to pay the remaining balance as a home loan to the builder.

Step 3. The builder in return agrees to pay interest on the buyer’s home loan. The process continues till the time of property possession by the buyer.

The chart below is an example of a Subvention Payment Plan of ATS Marigold (residential project in Gurugram) by ATS Infrastructure

Merits of SPP

It reduces the buyer’s EMI burden till property possession.

Transparency and discipline are assured as the builder is liable to pay interest on the buyer’s home loan and the bank ensures to get paid as per the extent of the construction work accomplished.

The builder is motivated to deliver the project on time.

Demerits of SPP

The builder may take advantage of the buyer's benefit of not having to pay loan interest by increasing property cost. As a result, the buyer ends up paying more than the actual cost of the property.

The chances of builder diverting the funds to other projects are also more and delaying the completion of the project of the buyer.

4. Flexi Payment Plan (FPP)

In Flexi Payment Plan, you will find mixed features of Construction Linked Plan and Down Payment Plan. You book the property with 10% payment, and 30%-40% of the total cost within 30 days of booking, similar to Down Payment Plan. The remaining 40%-50% balance is paid in the style of Construction Linked Plan, in instalments. The final 10% payment is required at the time of property possession.

The chart below is an example of a Flexi Payment Plan of Nirala Greenshire (residential project in Greater Noida) by Nirala

Merits of FPP

You get the benefit of two payment plans in a single scheme.

The amount paid as Down Payment in Flexi Payment Plan is almost half of what is charged in Down Payment Plan.

Demerits of FPP

Discounts given by the builder is usually 5%-6% in FPP whereas a 10%-15% discount is agreed on Down Payment Plan.